Alpha Investor: Sunday Nov 6, 2016

Summary

- Shell posted a massive turnaround in its bottom line last quarter on the back of an improved production profile, lower costs, and higher price realizations.

- Shell’s financial improvement is set to continue going forward as upstream oil price realizations will continue to improve on the back of a positive demand-supply environment in the oil industry.

- Oil demand has exceeded supply by 500,000 bpd this year and the trend will continue as the likes of Russia, Saudi Arabia, and the U.S. continue to reduce output.

- Shell’s focus on lowering both operating and capital costs will allow it to attain break-even point even if oil prices remain at $50/barrel, which will also improve cash flow.

On Tuesday last week, Royal Dutch Shell (NYSE:RDS.A) (NYSE:RDS.B) reported impressive results for the third quarter. In fact, Shell was able to achieve a major turnaround in its bottom line performance, posting a profit of $1.4 billion as compared to a huge loss of $6.1 billion in the same quarter last year. This impressive turnaround in Shell’s bottom line was a result of an increase in production as compared to the prior-year period, driven by the acquisition of BG that led to a favorable production mix in the upstream segment.

A closer look

More specifically, the upstream business of Shell performed commendably during the third quarter as it managed to attain break-even as compared to a loss of $600 million in the prior-year period. The majority of the improvement was driven by favorable volumes and production mix, as shown in the chart given below:

Meanwhile, favorable volumes in the gas segment due to the BP acquisition allowed Shell to keep its earnings in this segment constant at $900 million as compared to the year-ago period despite $400 million worth of write-downs and an identical drop in oil and gas price realizations. Hence, it is evident that Shell’s acquisition of BG has proven to be a tailwind for the company, especially because this move has increased Shell’s production by more than 22%, leading to growth in the bottom line.

In fact, due to the higher production on a year-over-year basis, Shell managed to improve its operating cash flow in an impressive manner. More specifically, it reported operating cash flow of $11.2 billion in the third quarter as compared to $8.5 billion in the year-ago period. Also, the company managed to increase its return on average capital employed to 6.1% as compared to 2.8% last year.

Therefore, it is evident that Shell has made a smart move by acquiring BG since this acquisition has effectively allowed it to enhance its production at a lower cost base. For instance, the above-mentioned increment in production has been achieved at a lower operating and capital cost base this year. This is shown in the chart given below:

As seen above, by the end of the year, Shell’s operating costs will be less than $40 billion as compared to almost $50 billion just two years ago. Additionally, Shell has reduced its annual capital expenses by $18 billion over the same time frame. Hence, Shell seems to have done the right thing by acquiring BG as this has allowed it to lower its costs and enhance production at the same time.

In fact, due to its lower costs, Shell is of the opinion that even if oil prices remain at $50 a barrel, the company will be able to achieve break-even earnings going forward. But, investors should not miss the fact that Shell has started witnessing an improvement in its oil and gas price realizations of late, which will complement the company’s focus on increasing production and lowering the costs.

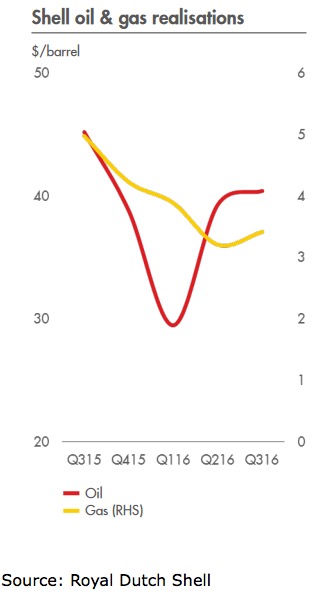

Shell’s realizations will gain steam

As 2016 has progressed, Royal Dutch Shell has witnessed an improvement in its oil and gas realizations. This is shown in the chart given below:

The improvement in oil and gas realizations at Shell is a result of the recent improvement in the price of these commodities. More importantly, it is likely that the price of both oil and gas will continue to improve going forward on the back of higher demand and lower production, which has led to a decline in oversupply in the industry.

In fact, lower supply and higher demand this year in the oil industry have resulted in excess demand of 500,000 barrels per day as compared to supply. Looking ahead, the trend of favorable demand and lower supply will continue due to the spending cuts witnessed in the industry in the past two years.

For instance, oil demand is set to remain consistently strong with an increase of 1.4 million bpd next year as compared to a rise of 1.5 million bpd in 2016. At the same time, global oil production will continue to take a hit, driven by lower output in key countries such as Saudi Arabia, Russia, and the U.S. More specifically, Saudi Arabia could lower its output by 350,000 barrels per day, while production in China and Russia could go down as much as 190,000 bpd and 220,000 bpd, respectively.

Similarly, oil production in the U.S. is set to go down by 600,000 barrels per day in 2016. As a result of these production cuts, the oversupply in the oil industry will come down as demand will continue to exceed supply. This is shown below:

Conclusion

Hence, a combination of an improved production profile, along with lower output and higher demand will continue to act as tailwinds for Shell going forward. The company did well last quarter as it managed to increase its earnings, and in light of the points discussed above, Royal Dutch Shell is on track to further improve its performance. So, investors should continue to hold the stock in their portfolios as the latest results indicate more upside going forward.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

This website and sisters royaldutchshellgroup.com, shellnazihistory.com, royaldutchshell.website, johndonovan.website, and shellnews.net, are owned by John Donovan. There is also a Wikipedia segment. EBOOK TITLE: “SIR HENRI DETERDING AND THE NAZI HISTORY OF ROYAL DUTCH SHELL” – AVAILABLE ON AMAZON

EBOOK TITLE: “SIR HENRI DETERDING AND THE NAZI HISTORY OF ROYAL DUTCH SHELL” – AVAILABLE ON AMAZON EBOOK TITLE: “JOHN DONOVAN, SHELL’S NIGHTMARE: MY EPIC FEUD WITH THE UNSCRUPULOUS OIL GIANT ROYAL DUTCH SHELL” – AVAILABLE ON AMAZON.

EBOOK TITLE: “JOHN DONOVAN, SHELL’S NIGHTMARE: MY EPIC FEUD WITH THE UNSCRUPULOUS OIL GIANT ROYAL DUTCH SHELL” – AVAILABLE ON AMAZON. EBOOK TITLE: “TOXIC FACTS ABOUT SHELL REMOVED FROM WIKIPEDIA: HOW SHELL BECAME THE MOST HATED BRAND IN THE WORLD” – AVAILABLE ON AMAZON.

EBOOK TITLE: “TOXIC FACTS ABOUT SHELL REMOVED FROM WIKIPEDIA: HOW SHELL BECAME THE MOST HATED BRAND IN THE WORLD” – AVAILABLE ON AMAZON.

{kind=link}